How to Foreclose One Credit Card EMI?

By OneCard | August 04, 2024

Taking out loans to fulfil your needs or dreams of owning a house, buying a car, or securing a quality education, is an age-old practice. These days, it is more common to apply for loans at banks or get personal loans via credit cards. Another common option is using the EMI (Equated Monthly Instalments) feature to make big-ticket purchases. EMIs allow you to stagger your large sum into smaller chunks to be paid across several months to over a year.

At any point during your EMI tenure, you can choose to foreclose the rest of the amount. This means paying off the rest of your due amount in one go and clearing the charge. For One Credit Card users, understanding how to foreclose credit card EMI can be a game-changer in optimising their financial health. Let us dive into the benefits and considerations of EMI foreclosure, as well as the process of foreclosing One Credit Card EMI.

Table of contents:

The Advantages of Credit Card EMI Foreclosure

While it’s not always a possibility, if you do get the opportunity to foreclose your EMI, it can be a clever financial decision. Here are some of the top advantages of EMI foreclosure:

1. Reduced Interest Payments

By settling your EMI ahead of its tenure, you cut down the total interest you would have paid over time. Essentially, you save money across your repayment tenure, which makes this a more cost-effective way to manage loans.

2. Improved Credit Score

Early repayment of EMIs is seen as a favourable sign when it comes to calculating your credit score. It shows credit bureaus that you are responsible when it comes to clearing your debt and paying your dues. Thus, foreclosing your EMI can lead to an improvement in your credit score.

3. Peace of Mind

While debt itself can enable bigger financial decisions that were previously impossible, it can also be an immense source of stress. As a result, foreclosing your EMI can offer a significant sense of achievement and peace of mind. Furthermore, knowing that you’ve cleared your financial obligations can boost your mental well-being.

ALSO READ: What Credit Card EMI & How Does It Work?

How to Foreclose Credit Card EMI on Your One Credit Card

Here is our step-by-step guide on how to Foreclose Credit Card EMI:

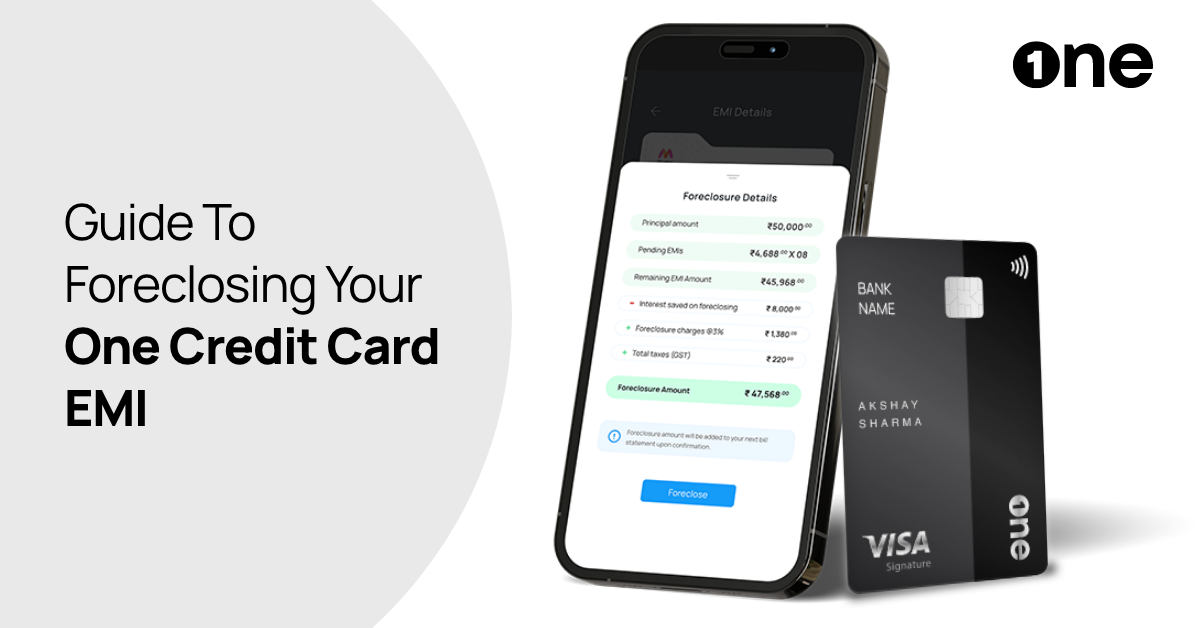

- Open the One Credit app and locate the EMI dashboard. This centralised hub offers a detailed view of your active EMIs.

- Select the EMI you wish to foreclose. You’ll see a comprehensive breakdown of the outstanding amount, including associated credit card fees and charges.

- Proceed with the ‘Foreclose EMI’ option. You can foreclose in just a few taps, making the process a simple one.

- Before you finalise the foreclosure, review all the charges associated with foreclosing your EMI. Typically, this will include a foreclosure charge – a percentage of the remaining principal amount, and the GST on this charge.

- Confirm foreclosure and clear your dues.

Things to Consider Before Foreclosing Your EMI

While foreclosing an EMI can be beneficial, it’s important to consider the financial implications, carefully. Firstly, you should compare the cost of the foreclosure charge and any additional fees against the interest you are saving to ensure that you are making a financially sound decision. Additionally, assess your overall financial situation to ensure that you can pay the foreclosure amount without putting a strain on your finances.

Now that you know how to foreclose your credit card EMI, you are equipped to decide whether to accrue more debt, carry your existing debt for longer, or close it out. Deciding to foreclose your One Credit Card EMI can be both a wise and forward-thinking financial move, as well as a mistake, if not thought out well. Use this knowledge to nurture healthier finances and easily leverage the One Credit Card app to navigate this process.

**Disclaimer: The information provided in this webpage does not, and is not intended to, constitute any kind of advice; instead, all the information available here is for general informational purposes only. FPL Technologies Private Limited and the author shall not be responsible for any direct/indirect/damages/loss incurred by the reader for making any decision based on the contents and information. Please consult your advisor before making any decision.

Sharing is caring 😉